Hi, this is Wayne.

Fear & Greed Index: 60

In the current market environment, if we observe only indexes performance, it is easy to arrive at an overly optimistic conclusion. The S&P 500 and Nasdaq continue to make new highs, with mega-cap technology stocks driving overall sentiment, giving the impression of stability and strong momentum. However, when we shift our perspective from price to structure, we begin to see that this “concentrated bull market” is not merely a result of sector rotation, but rather a transformation in the market’s pricing logic. Artificial intelligence is no longer just an industry theme—it is increasingly becoming the core of the market’s valuation framework. From semiconductors and cloud infrastructure to application layers and extended industries, capital continues to expand outward along the “AI narrative.” This expansion is not random, but follows a classic pattern in capital markets: the closer to the core, the stronger and more defensive the fundamentals; the further out, the lower the earnings visibility, but the greater the narrative potential—leading to more aggressive valuation expansion. This signals a fundamental shift in market logic. Investment decisions are no longer driven purely by fundamentals, but increasingly by narrative and expectations. As the market enters this phase, capital behavior also changes. Trades become more crowded, leverage increases, and prices are driven more by liquidity than by intrinsic value. Investors are no longer entering positions solely based on conviction, but increasingly out of fear of missing out.

This environment is not unfamiliar. In past market cycles, when capital continuously expands along a single dominant narrative, it often culminates in a future vision that is difficult to validate, yet highly compelling. Against this backdrop, major upcoming events—such as the IPOs of high-valuation technology, quantum computing, or space companies—should be viewed as stress tests for the entire valuation system. The real question the market must answer is whether these companies’ future scale and growth can justify current expectations. Once this question begins to be challenged, the impact will extend far beyond a single asset, affecting the entire narrative chain. This is precisely where risk accumulates. When earnings expectations become overly optimistic, when economic growth shifts toward investment-driven dynamics, and when interest rate uncertainty persists, any one of these variables can destabilize the current valuation foundation. Therefore, the key question is: within this structure—composed of narrative, capital, and expectations—which link will crack first? Because once confidence begins to weaken, market adjustments tend not to unfold gradually, but rapidly and violently. Before risks become explicit, the ability to identify direction and adjust early is the most difficult—and most critical—skill in investing.

For technical analysts, the goal is not to predict the market, but to establish a decision-making framework for navigating uncertainty. It is about whether one can, through systematic methods, identify potential turning points when structural changes begin to emerge. Whether through models, coding, parameter adjustments, or shifts in momentum, the objective is to respond accordingly—by reducing exposure, increasing cash positions, or reallocating portfolios. These actions are all forms of risk management. Ultimately, what matters is not who predicts the market most accurately. It is discipline. It is not about being right every time, but about avoiding being on the wrong side when structural turning points occur.

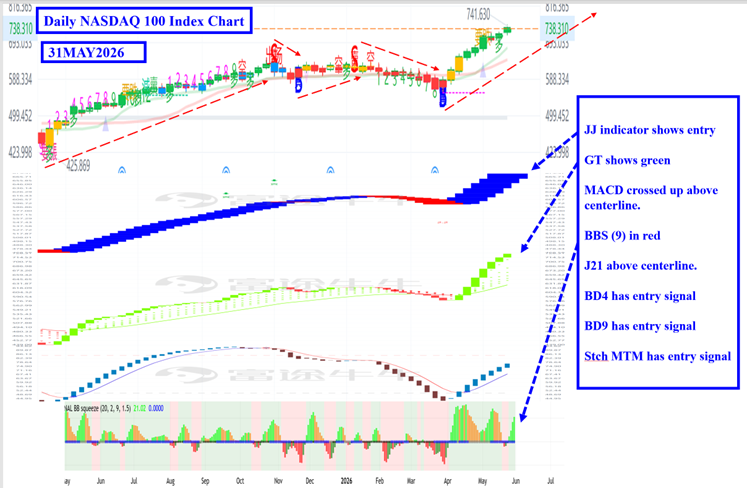

From the weekly chart perspective, the medium- to long-term trend remains upward. Within an uptrend, short-term pullbacks of smaller degrees are both normal and healthy.

On the daily chart, the trend is still upward, but technical indicators are showing overextended conditions. I expect there could be a short-term profit-taking phase in June, which would represent a healthy pullback. At that point, it will be important to observe whether to temporarily rotate into the G Fund or shift toward the S Fund with stronger SCTR score.

Stch MTM crossed up

100 % C fund (S&P 500)

please give will to: www.stjude.org/donatetoday

Leave a Reply

You must be logged in to post a comment.